![AI for Risk Assessment in Insurance [banner]](https://www.infopulse.com/uploads/media/aI-enabled-risk-assessment_1920x528.webp)

AI-Enabled Risk Assessment for Insurance Companies

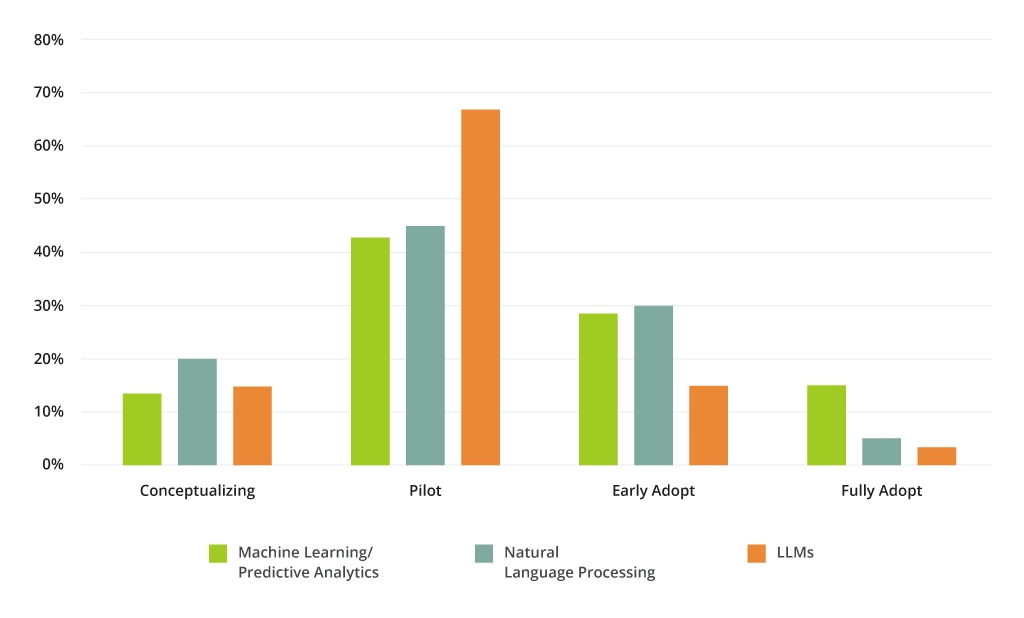

In 2024, 77% of insurance leaders are at some stage of adopting AI across functions, a 16 percentage point increase from 2023. If you’re also considering an investment in AI, here are the technologies and use cases we recommend looking into.

What Is AI-Enabled Risk Assessment?

AI-enabled risk assessment assumes using new technologies like machine learning, natural language processing (NLP), and big data analytics to process more data sources with higher accuracy and speed. Unlike traditional risk assessment techniques that mostly rely on structured historical data, AI technologies can also leverage unstructured data from a wider range of sources, perform analysis on real-time data, and provide more accurate predictive risk estimates.

AI technologies for risk assessment for insurance companies:

- Predictive big data analytics

- Natural language processing (NLP)

- Optical character recognition

- Machine learning (ML) algorithms

- Deep learning (DL) algorithms

- Large language models (LLMs)

Benefits of AI in Risk Assessment

Insurance carriers are dealing with an exploding volume of available data. Consumer health-tech wearables and connected medical devices provide healthcare insurers with high-fidelity data on clients’ health risks. ADAS and vehicle telematics data offer extra insights into drivers’ behaviors, while industrial IoT devices help to better understand equipment performance and track goods in transportation.

Yet, large insurances only analyze 12% of the data available to them, mostly due to inadequate technology foundations for effective big data analysis. Indeed, traditional business intelligence tools (BI) cannot query unstructured data — visuals, handwritten notes, or audio files. The lack of proper data processing pipelines, paired with an ad hoc approach to data science, in turn, limits the speed of structured data processing.

With the right technical foundations in place, AI models can process and analyze data 100 times faster than traditional methods, enabling real-time risk assessment. This speed and accuracy enable insurers to perform more granular and frequent risk assessments, to delight customers with faster responses and personalized policies. The risk system performance also improves over time as the model becomes exposed to more data.

Fundamentally, AI technologies can drive the following benefits for insurance companies:

- Enhanced data segmentation for a more granular analysis of risk factors

- Superior forecasting accuracy in complex risk analysis scenarios

- Real-time risk radar monitoring and alerting in areas of compliance

- Advanced threat and fraud detection with low false-positive rates

- Improved organizational productivity through the automation of menial work

- Faster decision-making thanks to dynamic insights and predictive capabilities.

5 AI Risk Assessment Application Scenarios

The insurance sector, as the financial services at large, has approached AI adoption with caution. ML and DL models are mostly deployed for automating operational processes and augmenting decision-making. Few (if any) insurance companies use AI to auto-execute prescriptive action, based on the produced risk evaluations.

AI risk assessment tools mostly provide insurers with data aggregation, curation, and analysis tasks, adding extra efficiencies to time-consuming processes like underwriting, claims processing, fraud detection, customer risk profiling, and compliance monitoring.

Augmented Underwriting

Policy underwriting is one of the key insurance processes where algorithmic automation can bring greater accuracy and efficiency. Traditional, rule-based risk-scoring models often fail to provide a comprehensive assessment to the underwriter, forcing them to conduct labor-intensive manual research. Underwriters spend roughly 70% of their time on non-core work, ranging from information lookup and administrative tasks to sales and customer support.

Artificial intelligence tools can help speed up a lot of repetitive tasks concerning data collection, aggregation, and analysis. Apart from mining a wider range of internal and external insurance data sources to create a present-day baseline, AI risk assessment tools can also evaluate historical data and link it with the current findings to create accurate predictive insights. AI-augmented underwriting allows professionals to concentrate their efforts on evaluating risks and drawing judgements, rather than conducting intensive research.

Daido Life Insurance developed a predictive AI model for medical claims underwriting. The system provides a preliminary automatic assessment, based on the applicant’s medical records and exam results, visualizing its decision-making process, so that human underwriters can verify its results.

Best Insurance, in turn, recently launched Incomeadora — a quote-and-buy platform for Accident, Sickness, and Unemployment (ASU) insurance that leverages AI for policy underwriting. The algorithm was trained on a database of claims data and cancellation patterns to identify behavioral factors that better predict claim propensity and duration for individual customers.

Enhanced Claims Processing

Claims processing is another labor-intensive process, oftentimes ridden with inefficiencies due to siloed communication, limited data access, and lack of effective tools for document assessments. Intelligent automation solutions, powered by technologies like optical character recognition (OCR) and natural language processing (NLP), can speed up data extraction from claim forms, medical records, and repair invoices.

AXA uses NLP models to streamline the review of property risk engineering surveys, reducing processing time by over 50%, and improving risk selection. The insurer has also developed a secure risk management platform that helps its global clients monitor their assets and take proactive steps to minimize the impacts of natural disasters, supply chain disruption, and cyber threats.

Allianz Commercial, in turn, deployed an AI-enabled tool to speed up the processing of marine claims in North America. Neptune automates the assignment of claim cases to adjusters using real-time information on their workload and provides real-time KPIs to claims managers. Previously, the process was done manually, resulting in delays and suboptimal work distribution.

Fraud Detection and Prevention

Machine learning has already proved its mettle for fraud detection in the financial services and telecom — and the technology can also tilt the scale in the insurance sector. Fraud occurs in about 10% of property and casualty (P&C) insurance losses, while false and fraudulent claims in healthcare cost companies $3.1 billion, according to Coalition Against Insurance Fraud.

Algorithms can help cross-check submitted claims for inconsistencies and help detect fraudulent submissions. For example, identify deepfakes of medical records or altered images of property damage. Zurich Insurance says it employs a range of fraud models with AI components to detect fraud across markets and divisions.

Shift Technology, for example, has trained its insurance fraud detection models on millions of data samples — claims, first notice of loss, pictures of damages, and other assets. Significant model exposure to a variety of fraud scenarios makes it more accurate than traditional systems. The system delivered an 87% hit rate of alerts for one of the company’s insurance clients — well above the industry average of 30%. This has led to a recovery of £44.5 million and a further £54 million blocked before payment.

High accuracy rates are driving more leaders to adopt AI. By 2026, 83% of anti-fraud professionals from across industries intend to use AI-powered tools.

Improved Risk Profiling

AI enables more granular risk assessments by evaluating individual risk profiles rather than relying on broad, pre-programmed categories like age, income, or employment status. What’s more, real-time risk data processing with AI enables insurers to offer more innovative products.

Globally, 60% of consumers are interested in usage-based auto insurance — policies, adapted to their driving behaviors and vehicle usage trends. US carrier Allstate was the first major insurer to introduce a telematics-based product in 2020, which has since grown at a CAGR of over 15%. By agreeing to share their driving data, Allstate policyholders benefit from more favorable rates. Drivewise gives drivers insights into their on-the-road behavior, promoting safer driving. Data from Drivewise is used each year to adjust premiums.

Italian Generali also offers tailored pay-how-you-drive policies that reward safer drivers with lower premiums. In the home market, the company launched an AI-enabled driver assistant, providing real-time coaching to drivers.

Automated Compliance Monitoring

A greater degree of automation can also help reduce the lag between regulatory changes and institutional compliance in the insurance sector. German insurance companies spend between 4% and 7% of their annual personnel and material expenses on regulatory compliance.

NLP tools can be used to monitor the latest regulatory developments and extract relevant updates on new control requirements and then cross-map current policies and procedures against regulatory requirements. Advancements in generative AI also enable better audio and visual data processing, as well as automatic summarization and text classification by topic or sentiment.

Intelligent automation systems can be used to draft regulatory reports, prefilling and cross-validating data from connected sources. Backoffice monitoring systems, in turn, can help detect cases of non-compliance for faster issue resolution.

Challenges and Considerations When Using AI for Risk Assessments in Insurance

The enthusiasm around AI in the insurance sector has certainly been high, yet not all leaders are actively investing in this area. A NAIC Life Insurance AI/ML Survey found that among the 42% of insurers who are not using or exploring AI/ML, claim that the key reasons are ‘lack of a compelling business reason’, ‘lack of resources and expertise’, and ‘legacy IT systems’.

Beyond the internal reasons, there are also external market factors that insurers must consider — compliance with the emerging AI legislation around model fairness, accuracy, and explainability. AI systems also require appropriate cybersecurity protection mechanisms to avoid becoming a costly liability.

When considering AI risk assessment model implementation, you should always consider:

- Data availability. Insufficient or inaccessible data for model training and validation will lead to eschewed outputs. AI system adoption requires a mature data management and governance architecture to ensure compliant generation of training datasets.

- Model accuracy. Algorithm performance accuracy depends on the quality and variety of training data, as well as the selected training methods. Performance drift can also occur over time if the distribution of data changes over time or the business context evolves. Monitoring must be in place to detect drift at the onset.

- Model explainability. The produced results must be transparent and fair or else insurers risk significant financial and reputational losses. Explainable and ethical AI systems provide the rationale behind AI-generated outcomes and can be easily audited for mistakes and biases.

Conclusion

The insurance sector is known for being conservative when it comes to emerging technologies. Indeed, AI adoption should be approached with a heavy dose of skepticism as there are a lot of tangible limits to the current systems’ capabilities. Yet, what modern AI systems for risk management can do effectively is help process wider reserves of data to augment underwriting, streamline claims processing, and enhance fraud detection.

![Generative AI and Power BI [thumbnail]](/uploads/media/thumbnail-280x222-generative-AI-and-Power-BI-a-powerful.webp)

![Data Governance in Healthcare [thumbnail]](/uploads/media/blog-post-data-governance-in-healthcare_280x222.webp)

![IoT Energy Management Solutions [thumbnail]](/uploads/media/thumbnail-280x222-iot-energy-management-benefits-use-сases-and-сhallenges.webp)

![Carbon Management Challenges and Solutions [thumbnail]](/uploads/media/thumbnail-280x222-carbon-management-3-challenges-and-solutions-to-prepare-for-a-sustainable-future.webp)

![Automated Machine Data Collection for Manufacturing [Thumbnail]](/uploads/media/thumbnail-280x222-how-to-set-up-automated-machine-data-collection-for-manufacturing.webp)

![Pros and Cons of CEA [thumbnail]](/uploads/media/thumbnail-280x222-industrial-scale-of-controlled-agriEnvironment.webp)