![White-label Mobile Banking App [MB]](https://www.infopulse.com/uploads/media/banner-1920x528-white-label-mobile-banking-application.webp)

White-Label Mobile Banking: A Look at Benefits and Concerns

- Banking & Fintech

- Business Applications

- Digital Transformation

- Software Engineering

- Digital Experience

Today, mobile banking apps are widespread, allowing us to ditch trips to the ATM and manage our finances on the go. From checking balances and transferring funds to paying bills, these apps offer much-needed convenience. But behind the scenes, a new approach is transforming how they are built: white-label applications.

A recent study by Juniper Research predicts the number of digital wallet users to surpass 5.2 billion globally by 2026. This rise highlights the growing appetite for user-friendly mobile payment solutions. White-label mobile banking apps, often incorporating digital wallet functionalities, are well-positioned to address this evolving user preference.

Benefits of White-label Mobile Banking Apps

Think of a white-label app as a pre-built mobile banking shell. A wide range of financial and more often non-financial institutions from established names to neobanks (also known as challenger banks or digital banks that operate exclusively online, typically through mobile apps) utilize these platforms. By tailoring these apps with their own branding and features, any organization can offer a modern mobile banking experience with frictionless UI/UX. Faster time-to-market is guaranteed in this case since there is no need in the hefty upfront investment of building an app from scratch. The overall agility of a white-label platform allows capturing a significant share of the burgeoning digital banking user base.

Here are other benefits white-label mobile banking apps extend to:

- Uninhibited growth with scalability

- Reduced costs and faster launch

- Data-driven decisions with integration and analytics

- Increased customer engagement and market reach

- Secure and compliant from the ground up

- Improved brand differentiation through customization

Case in point: Large Nordic Banks can now experience most of these benefits with their own white-labeled mobile banking apps. First, Infopulse developed a native iOS/Android custom mobile app, then customized it for over 10 Nordic banks. This project demonstrates how pre-built platforms can significantly reduce development time and costs while still creating secure and feature-rich mobile banking apps.

How Non-Financial Institutions Can Advance with White-Label Apps

Driven by the ever-increasing focus on customer retention and mobile adoption, the white-label app market is poised for significant growth in the coming years. This trend aligns perfectly with the broader rise of open banking, projected to reach $75.7 billion by 2028. While open banking unlocks new possibilities, the benefits of white-label solutions extend to non-financial institutions (NFIs) too.

Ways NFIs are embracing white-label solutions:

- Retailers can use pre-built white-label loyalty apps with features like points systems and reward management. This allows for the launch of engaging loyalty programs in a timely and efficient manner.

- Telecom providers can utilize white-label solutions to build upon their established bill payment services offered directly through their networks, which opens doors to new revenue streams.

- E-commerce platforms benefit from white-label solutions by allowing the platforms to seamlessly integrate secure payment gateways directly into their platforms. By eliminating the need for customers to navigate to external payment pages, you can reduce cart abandonment rates.

- Insurance companies can leverage white-label solutions to offer premium financing, allowing customers to pay for insurance premiums in installments rather than a large upfront sum.

Modernizing Legacy Systems with White-label and BaaS

Legacy IT systems can often hinder a bank's ability to keep pace with innovation, as highlighted in the EY report: "BaaS (Banking-as-a-Service) allows banks to access innovative solutions and capabilities without the need for significant upfront investment or ongoing maintenance." This is where BaaS comes into play.

Traditionally, banks and fintech companies operated separately: banks held licenses and infrastructure for core financial services, while fintechs brought innovation and agility. BaaS creates a bridge between these two entities, fostering a win-win scenario.

As a cloud service model, BaaS allows financial institutions to share the core functionalities of their banking systems like account management and payments through APIs (application programming interfaces) with almost any third-party businesses. The latter can then leverage this modern infrastructure to offer branded mobile banking apps, built on modern, scalable cloud platforms with microservices and data analytics. White-label mobile banking platforms capitalize on this by offering customizable app solutions that easily integrate with various BaaS providers without the need for extensive in-house development.

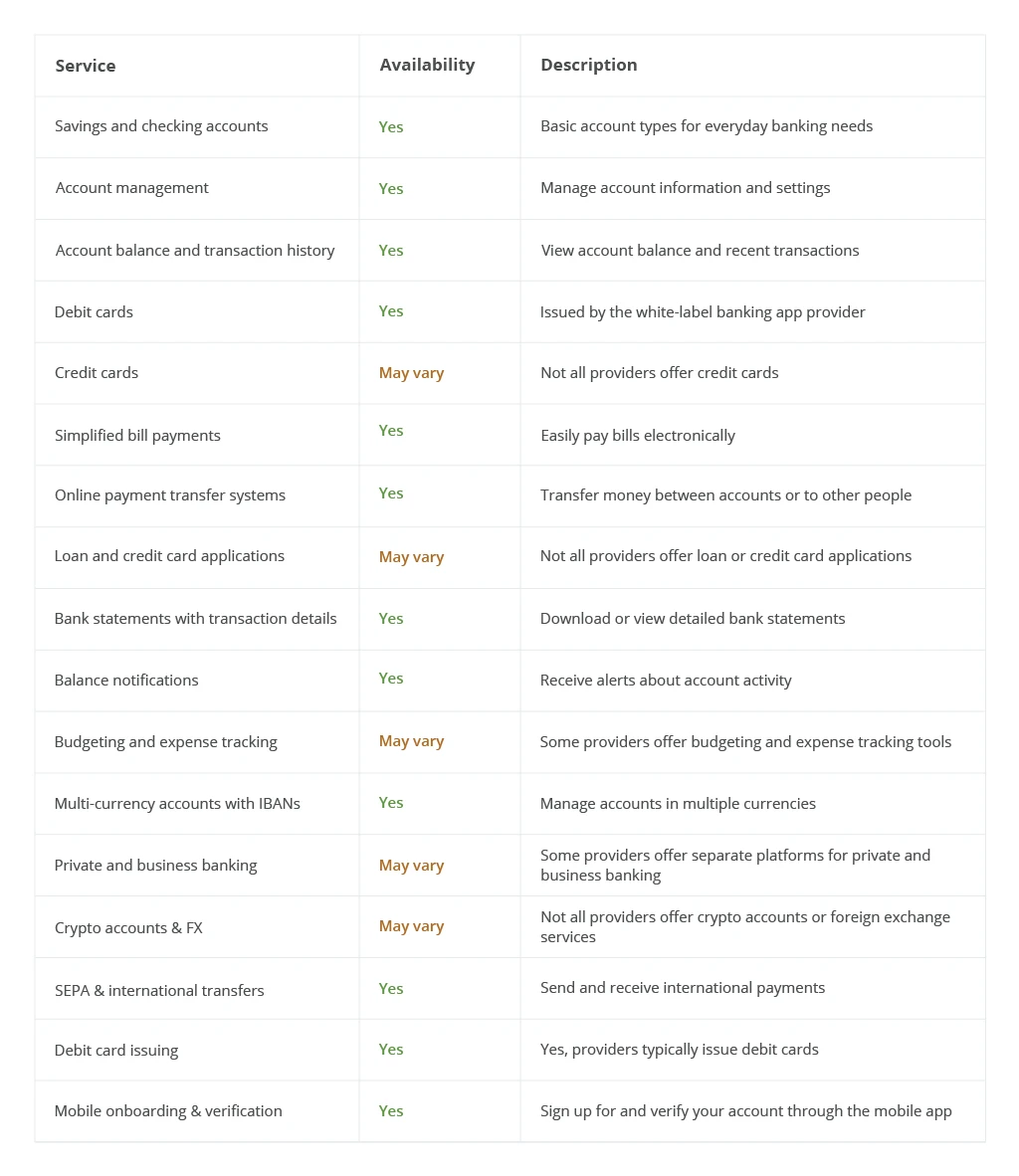

Common White-Label Mobile Banking Services

Private-label banking app providers offer digital finance players a comprehensive suite of financial services through a single platform, thus simplifying integration. The table below details the commonly available services:

While the data above highlights core functionalities, some white-label providers offer additional features to enhance user experience. These may include:

- Onboarding carrousel

- Account dashboard

- Mandate switch

- Different permissions / roles

- Statements, transactions, payment types

- Repeat and reply to payments

- Payment confirmation and approval

- Manage limits and settings

- Mobile wallet

- Card freeze/terminate, Manage PIN and CVV

- Virtual cards

Do you already have a well-functioning app? Integrate it with your existing systems for a frictionless customer experience. Infopulse, with its proven track record in connecting applications, systems, and services into a unified IT ecosystem, can help you exploit the full potential of Banking-as-a-Service.

White-label Banking Adoption Concerns

While white-label mobile banking offers direct gains, banks integrating with BaaS APIs might have some technical anxieties. These concerns arise due to the distributed nature of fintech banking solutions, where functionalities are delivered through a third-party platform. Here are the key areas that need attention:

- API security and integration: BaaS integrations require multi-factor authentication, ongoing API monitoring, and compatibility management to secure data and ensure smooth operation despite frequent API updates by the provider.

- Data residency and compliance: Data residency regulations like GDPR limit data movement, so banks using BaaS need to confirm data location and ownership to comply with KYC/AML and their own internal security standards.

- Limited control and visibility: Limited control over the underlying platform can hinder a bank's ability to maintain brand consistency in the white-labeled app and troubleshoot potential security issues due to a lack of visibility into the BaaS provider's internal operations.

Fortunately, just as banks can establish guidelines for third-party app developers, similar strategies can be implemented to maintain control over the user experience within a white-labeled mobile banking app.

How to Maintain Control in a White-Label World

When banks allow third-party apps to leverage their APIs, some control over the user experience is relinquished. A poorly designed app can negatively impact the bank's brand. Here's how banks can maintain control:

- Establish clear guidelines for developers, outlining security, functionality, and UX standards that all third-party apps must meet.

- Before launch, banks should have a thorough app review process to ensure all third-party apps meet their standards.

- Continuously monitor the performance of third-party apps to identify and fix issues that could negatively impact user experience.

While we can’t completely eliminate open banking security concerns, we can capitalize on a treasure trove of opportunities it presents. Financial players, like neobanks, and non-financial organizations (retailers, telecoms, startups, etc.) can build a white-label application on open APIs for personalized payment experiences. Such an app may come with innovative features and often lower fees because of lower overhead and competitive rates.

So, let's take a closer look at a successful example of a white-label mobile banking app in action. In the Netherlands, major bank ABN Amro developed their new app called Grip based on a white-label banking platform. Its standout feature allows users to manage finances in one place, even if they have accounts with different banks. What’s more, users can connect up to five existing accounts and view them all in one place. 75% of new users recommended it, and half gave ABN Amro a high rating, proving the value of white-label banking.

Conclusion

White-label mobile applications offer a powerful and cost-effective solution for financial institutions of all sizes. By drawing on pre-built platforms and BaaS technology, institutions can quickly launch modern mobile banking apps without the burden of extensive development. This not only reduces costs but also stimulates collaboration between traditional banks and innovative fintech companies. As the demand for mobile banking continues to rise, white-label solutions are set to play a key role in shaping the future of convenient financial management.

![Deepfake Detection [Thumbnail]](/uploads/media/thumbnail-280x222-what-is-deepfake-detection-in-banking-and-its-role-in-anti-money-laundering.webp)

![Data Analytics Use Cases in Banking [thumbnail]](/uploads/media/thumbnail-280x222-data-platform-for-banking.webp)

![Mobile Banking Trends [Thumbnail]](/uploads/media/thumbnail-280x222-mind-your-app-why-reinventing-mobile-banking-really-matters.webp)

![AI and RPA Integration for Banking [Thumbnail]](/uploads/media/thumbnail-280x222-ai-and-rpa-integration-for-banking-possibilities-of-intelligent-automation.webp)

![Banking Software Development [Thumbnail]](/uploads/media/thumbnail-280x222-software-development-out-of-the-box-vs-custom-vs-low-code-solutions.webp)

![API as a Product in Banking [thumbnail]](/uploads/media/thumbnail-280x222-business-opportunities-of-api-products-in-banking-and-finance.webp)

![Overview of Connected Banking and its Benefits [thumbnail]](/uploads/media/what-is-connected-banking-its-promises-and-benefits-280x222.webp)

![Low-code for Banking [thumbnail]](/uploads/media/thumbnail-280x222-low-code-benefits-use-cases-banking.webp)

![API Strategy for Banking [thumbnail]](/uploads/media/whys-and-hows-of-api-strategy-for-banking-280x222.webp)

![Digital Customer Engagement in Banking [thumbnail]](/uploads/media/a-complete-checklist-for-enhancing-digital-customer-engagement-in-banking-280x222.webp)

![Open Finance vs Open banking [thumbnail]](/uploads/media/how-open-finance-extends-capabilities-of-open-banking-280x222.webp)